Introduction

July 2024 marks the first time since 2016 that USDA’s National Agricultural Statistics Service has not published its July Cattle Inventory report, which would typically come out this week and contain data about the size of the calf crop, which producers and analysts would use to gauge if the cattle inventory is expanding, contracting or holding steady. In an announcement in April, NASS cited budget constraints as the reason for cancelling this report along with county level production and yield data and the objective cotton yields survey.

The 2024 cattle inventory is the lowest it has been since 1951, which has sent beef prices soaring. The hog industry is looking profitable, too, but has a lot of ground to make up for with last year’s losses as well as supply chain complications caused by California’s Proposition 12. Poultry including eggs, broilers and turkeys are continuing to contend with Highly Pathogenic Avian Influenza (HPAI). This Market Intel will use data from several USDA reports to assemble the market outlook for animal proteins for the second half of 2024.

Cattle

Supply

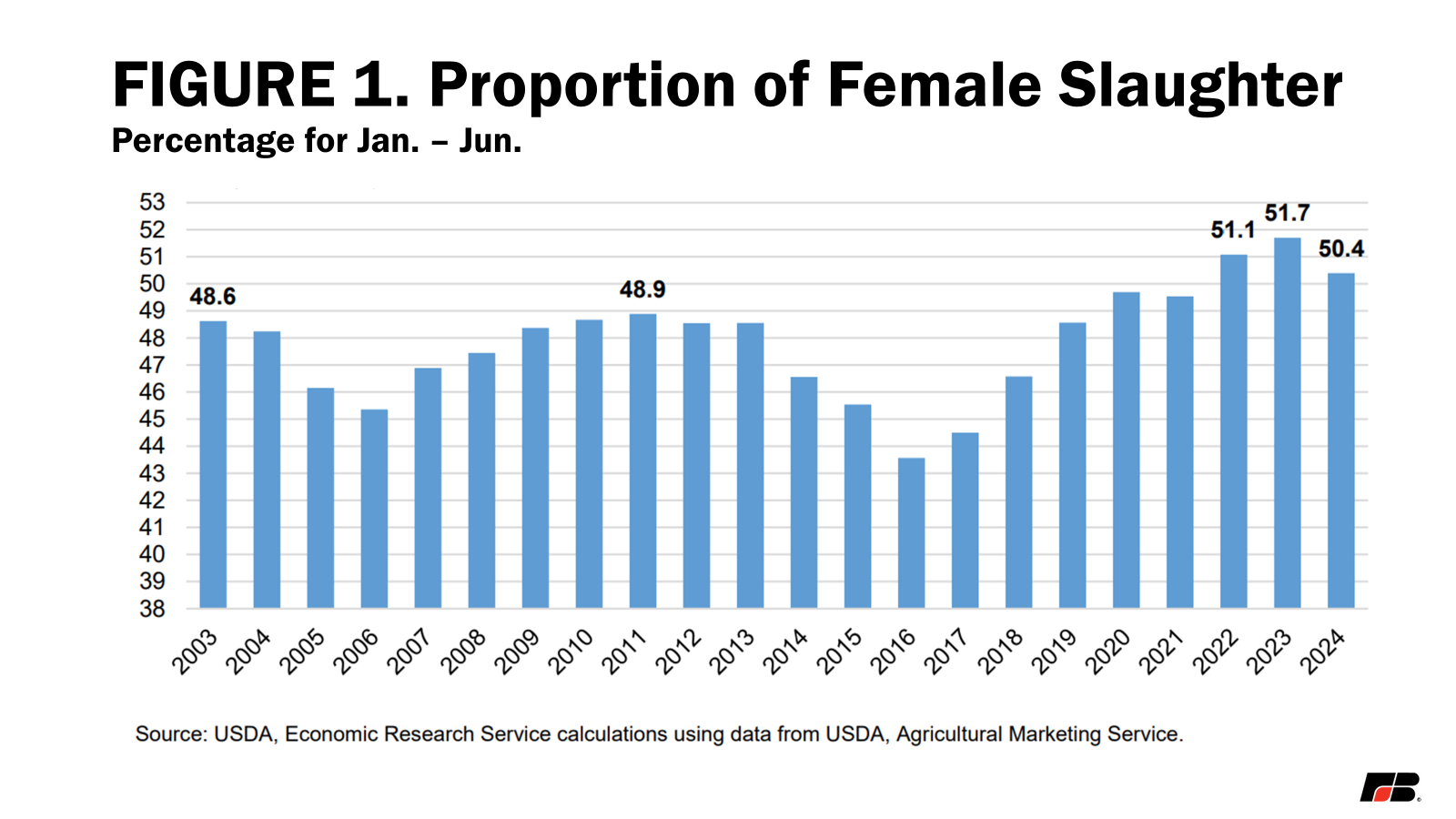

USDA estimated in its January Cattle Inventory report that all cattle and calves in the United States were 87.2 million, the lowest since 1951. The country’s cattle producers, facing stress from multiple years of drought and high supply costs, have been marketing a lot of cows and heifers since 2020 (Figure 1), so fewer of these female cattle are available to produce calves. USDA’s July Cattle Inventory previously provided a breakdown of the U.S. cattle inventory including the calf crop for the first half of the year. Without this report in 2024, it is much more difficult to estimate what cattle supplies look like for the remainder of the year. Farmers and stakeholders will have to wait until January to receive this data. In the meantime, analysts will be using what they do have available to piece together the overall market outlook.

Feedlot inventories are slowly reflecting the lower cattle inventory. In its July Cattle on Feed report, USDA estimated all cattle and calves on feed in the United States was 11.3 million on July 1, up 1% from a year ago. Heifers and heifer calves accounted for 4.48 million head. While this is up only slightly, this is near the record-high number of heifers and heifer calves for the July 1 report and makes up about 40% of the overall cattle on feed. Historically, heifers make up around 32% of the overall cattle on feed. This is a strong indicator that farmers are still not withholding heifers to rebuild the U.S. cattle herd.

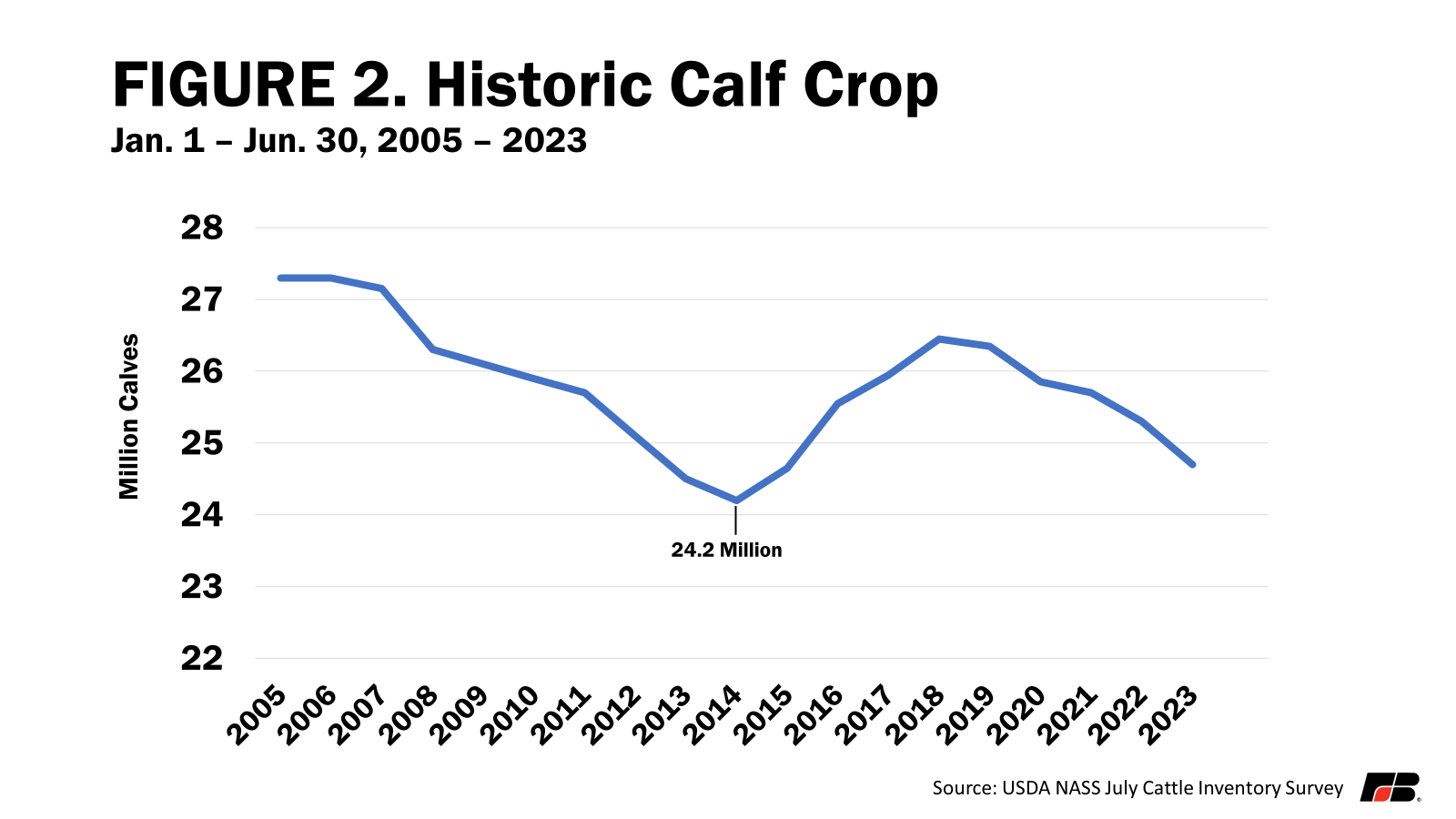

One particularly important metric the July Cattle Inventory would have provided is the size of the calf crop for the first half of the year. This is the time when most of the U.S. calf crop is born. It takes about a year for a heifer calf to reach maturity for breeding. These calves that could be replacements will not reach breeding age until 2025. The first opportunity for herd expansion will be possible if farmers begin to withhold heifers from this year’s calves for breeding in 2025. This means the arrival of the 2026 calf crop will be the first opportunity on the horizon to increase the cattle inventory. The 2023 July Cattle Inventory report estimated a Jan. 1 – June 30 calf crop of 24.7 million head (after later adjustments, see Figure 2). The record-low calf crop since the July Cattle Inventory survey began is 24.2 million in 2014. A drop of just 2% from last year’s calf crop would tie the record low. Addressed earlier, it is apparent that a high number of female cattle are still being placed on feed for slaughter rather than being withheld for breeding purposes. This means that a record-low calf crop for the first half of the year is possible.

Demand/Prices

Summer demand has helped push prices up. Choice grade beef has worked its way above $300/cwt and was up $1.04 on July 29 at $314.81. On the same day select grade was up $4.06 at $301.52/cwt. Something that can be helpful in gauging the demand for beef is the difference between choice and select grade beef. A wider difference between choice and select beef often indicates a consumer is willing to pay more for premium cuts of beef where a narrowing difference may show that consumers are more willing to settle for a lower quality cut. The current spread sits at $13.11, which is just below the year-over-year average of $16.08. This spread has been widening since late March, which is typical when the grills come out for warmer spring and summer months. July average cash fed steer prices have ranged from $188/cwt to $192/cwt. As we approach fall, cattle available for placements on feed should slow down. This should bring higher cash prices at the sale barn, which will drive beef prices higher as well.

Summary and Conclusions

Livestock markets for the second half of 2024 are a mixed bag. Shrinking cattle supplies along with strong beef demand will keep cattle and beef prices strong through 2024 and likely through 2025. Hog producers have had some relief from last year’s losses but still face considerable obstacles to maintaining profitability as production is forecast to increase through the remainder of the year. The poultry industry is facing risks associated with HPAI, adding uncertainty as we soon transition to fall when migratory birds begin their annual trip south.

While profitability in livestock is holding for now, there are still obstacles on the horizon including rising costs of production and a down ag economy. All sectors of animal agriculture are relying on tools from an outdated farm bill that may not provide the safety net needed for long-term sustainability. This jeopardizes not only the continuity of many farms in the United States, but their ability to continue growing the affordable food, fiber and renewable fuel that people throughout the world rely on.

{kind=link}