Source: USDA

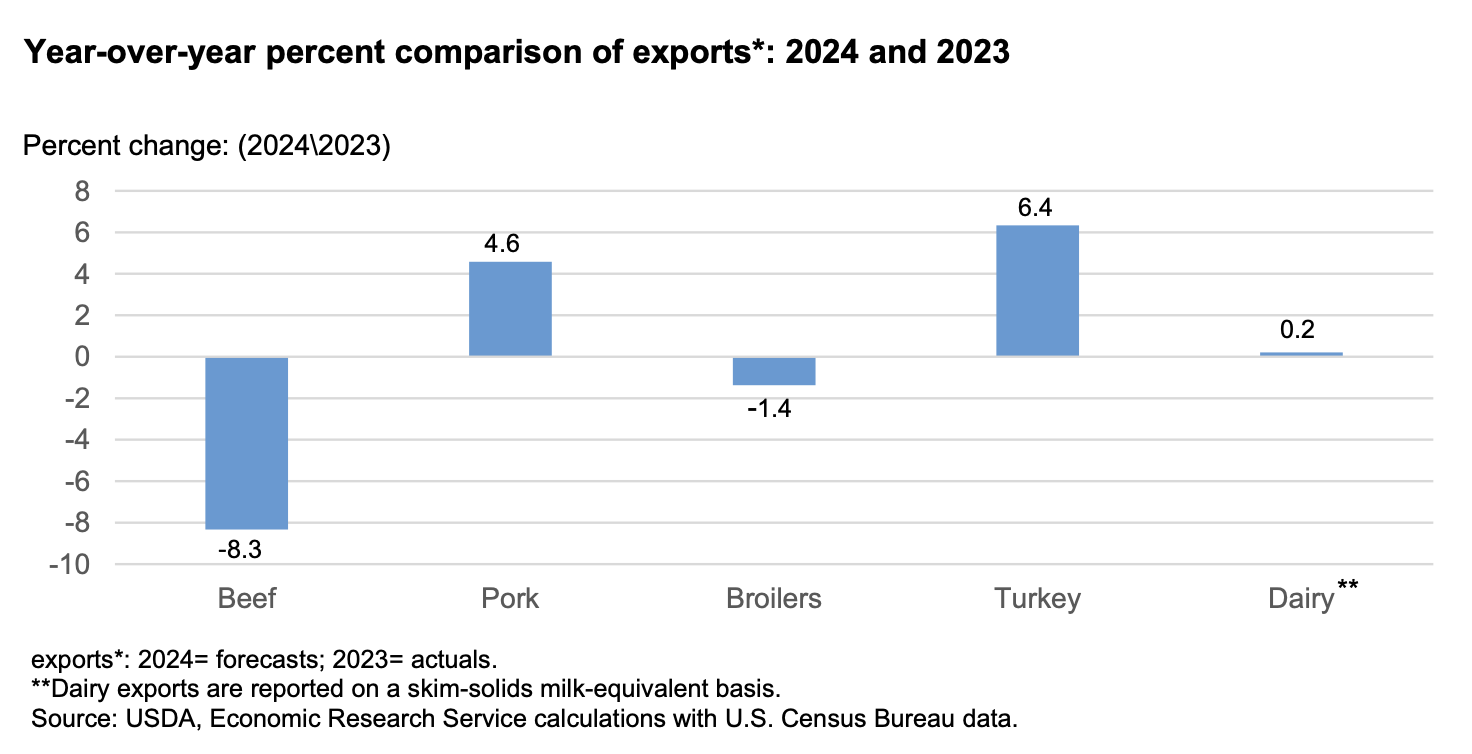

Anticipated percent changes in 2024 red meat, poultry, and dairy exports compared with 2023

U.S. export forecasts for red meat, poultry, and dairy for 2024 compared to actual export data from 2023 are presented below in a percent-change format. In 2024, beef exports are expected to be about 8.3 percent lower than those of 2023 due to lower 2024 beef production from tightening cattle supplies, as well as from tougher global competition from such beef exporting countries as Australia. Pork exports are forecast to increase almost 4.6 percent over 2023 due to higher domestic production and less global competition from the European Union. Broiler exports in 2024 are expected to decline about 1.4 percent compared with last year, due to higher domestic prices and weak demand from China. Turkey is expected to be competitively priced in 2024, with exports forecast to be up 6.4 percent compared with 2023. Compared with 2023, dairy exports on a skim-solids milk-equivalent basis should increase slightly this year—about 0.2 percent. Relatively strong domestic demand for dairy products and limited growth in milk production will likely limit export growth.

Summary

Beef/Cattle: Based on slaughter data through early March 2024, the projection for cow slaughter is raised in the first half of the year and fed cattle marketings are shifted out of the first quarter and into the outlying quarters at a more rapid pace. As a result, the forecast is raised by 140 million pounds to 26.325 billion pounds. Cattle prices are raised on firm demand and recent price data. The forecast for beef imports in the first quarter is raised 50 million pounds to 1.200 billion pounds. Projections for beef exports are unchanged from last month.

by: Russell Knight and Hannah Taylor

Fed Cattle Supplies Remain Larger Than a Year Ago

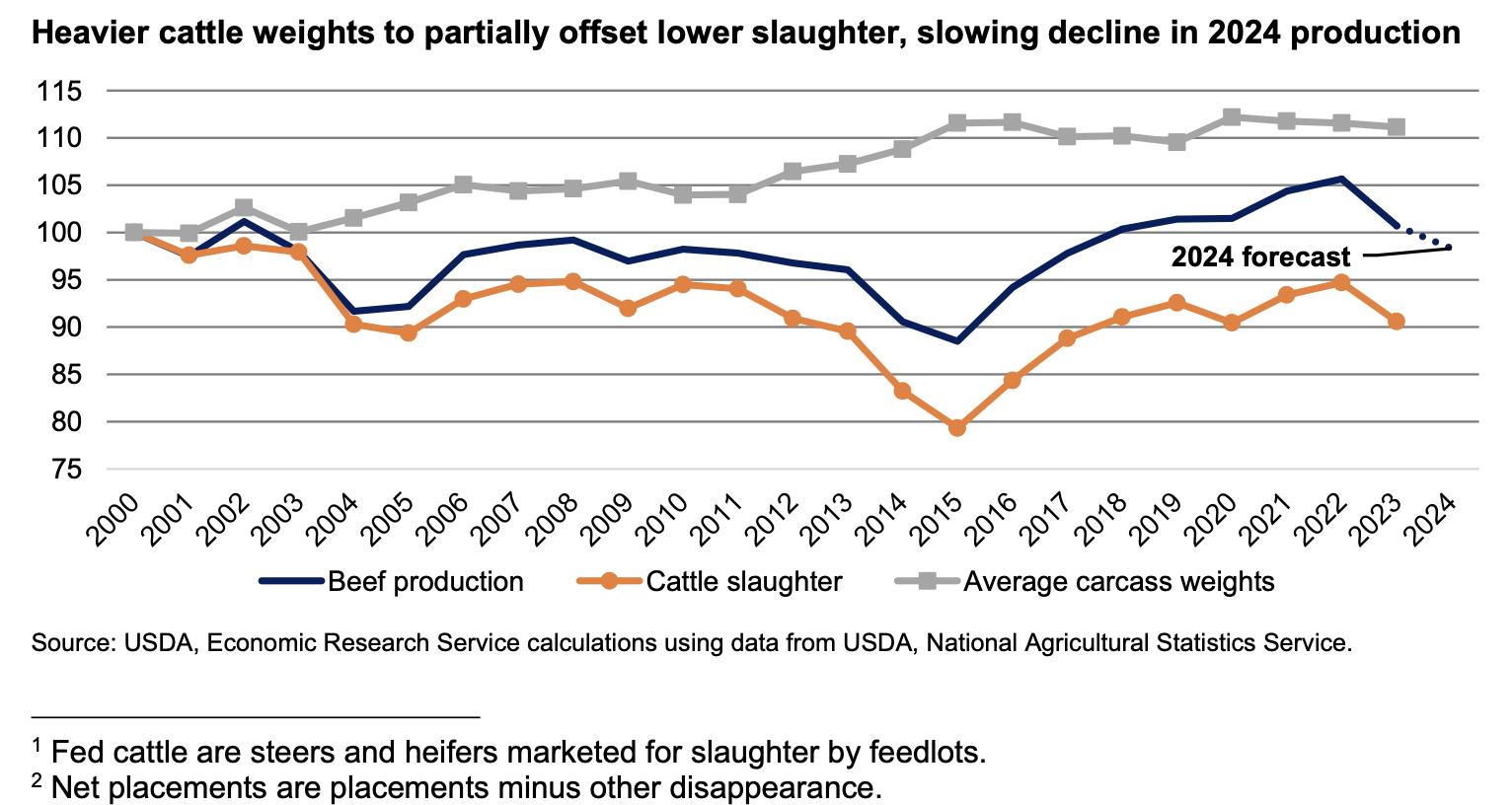

The January Cattle report noted year-over-year declines in all classes of cattle, with a significant reduction in the number of calves available on January 1 for feedlots, stockers, and backgrounders to purchase this year. This will lead to a sharp decline in the number of calves placed in feedlots as the year progresses, and declines in beef production will likely be more noticeable in late 2024. Despite declines in the number of cattle on January 1st, a slower pace of fed cattle1 slaughter is accumulating market-ready supplies in feedlots.

The latest Cattle on Feed report, published by USDA, National Agricultural Statistics Service (NASS), showed a February 1 feedlot inventory of 11.797 million head, just slightly above 11.754 million head in the same month last year but down 1 percent from January. Feedlot net placements2 in January were almost 9 percent lower year over year at 1.711 million head. Marketings in January were 1.844 million head, nearly on par with last year but reflecting an additional slaughter day. On February 1, the number of cattle on feed over 150 days was up 6 percent above year-ago levels.

This increase of market-ready supplies of fed cattle is likely driven in part by feedlots attempting to maximize poundage per animal, along with packers reducing slaughter schedules to maximize operational efficiencies as their margins are under pressure from paying much higher prices for fed cattle. As those measures are keeping cattle in feedlots longer, fed cattle are being processed at heavier weights than a year ago, partially offsetting lower total slaughter this year. Overall, beef production this year is expected to be 2 percent below levels in 2023, which is a slower decline than from 2022 to 2023, as shown in the chart below.

2024 Production Forecast Raised on Slightly Higher Slaughter

The production outlook for 2024 is up marginally by 140 million pounds from last month’s forecast to 26.325 billion pounds. This is based on a temporal shift of fed cattle marketings out of the first quarter and into the later quarters. Further, there is an expectation of higher cow slaughter (females that had a calf) in the first half than anticipated last month, likely supported by the surge in cull cow prices.

The forecast for first-quarter beef production is lowered by 120 million pounds from last month. From last month’s expectation for first-quarter slaughter, the pace of fed cattle slaughter has been much slower, but it was partially offset by a faster pace of cow slaughter. Further, anticipated bull slaughter was adjusted slightly lower on weekly slaughter data. In the second quarter, the forecast for beef production is increased 145 million pounds from last month. This is the result of shifting a portion of fed cattle marketings from the first quarter to the second quarter. Anticipated cow slaughter in the second quarter was adjusted higher based on the pace of beef cow slaughter in the first quarter and strong cull cow prices. In the third and fourth quarters, production is forecast up 40 and 75 million pounds, respectively, from last month, with marketings pushed into the second half as higher forecast fed cattle prices are expected to encourage feedlots to market cattle more aggressively.

Cattle Prices Raised on Firm Demand

In February, the weighted-average price for feeder steers weighing 750–800 pounds at the Oklahoma City National Stockyards was $241.37 per hundredweight (cwt), a $15.38 increase from January and about $57 above February 2023. The feeder steer price reported on March 11 reached $249.15 per cwt, almost $62 above the same week last year. The outlook for feeder calf prices is improved from lower projected market-year average corn prices and higher projected fed cattle prices from last month, as well as recent supporting price data. These factors support raising the forecast for each quarter by $5 for an annual average feeder steer price of $254.00 per cwt, a projected increase of 16 percent from last year.

The February average price for fed steers in the 5-area marketing region3 was $181.10 per cwt, $6.65 higher than January and more than $20 above February 2023. For the week ending March 10th, prices averaged $185.12 per cwt, up almost $20 from the same week last year.

Fed cattle carcass weights are heavier than a year ago, which is expected to persist for the remainder of the year. Given the price of wholesale boxed beef, packers have less incentive to pay even higher prices to pull cattle out of feedlots at a quicker pace. As forecast, packers are anticipated to pay more for fed cattle as the year progresses, when market-ready supplies tighten further. Based on recent price data, fed steer prices are raised across the quarters for a 2024 projection of $183.00 per cwt.

U.S. Beef Exports Less Competitive Globally

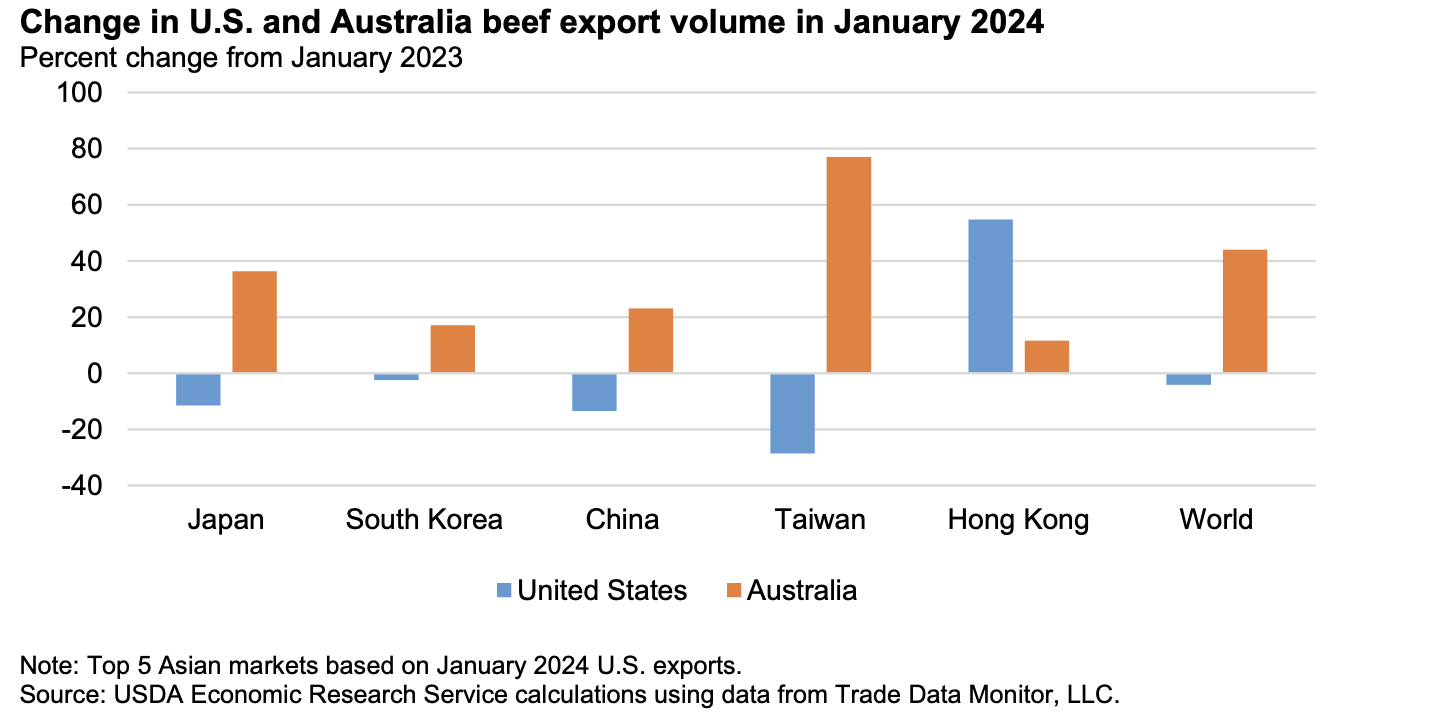

Monthly exports in January were 233 million pounds, 4 percent less than last year and 8 percent below the 2019–23 average. Exports to China were about 4 million pounds lower year over year, a 12-percent decrease, but were about mid-range of where monthly exports have been since ramping up in 2020. Exports to Taiwan were also 4 million pounds less than last year, though for a much smaller market this was about a 28-percent decrease. Exports to Japan were 11 percent lower year over year, while exports to South Korea were 3 percent lower. Reduced exports to Asia were partially offset by a 17-percent increase in exports to Mexico, where the peso continues to strengthen against the U.S. dollar, making U.S. beef more competitive.

On a global scale, U.S. beef is expected to continue to be less competitive, especially as Australian beef production increases. Australia has finally emerged from the rebuilding phase of the cattle cycle, and its production continues to increase. There are some indicators of drier weather across the country, leading producers to retain fewer cattle in order to maintain feed availability. According to the Australian Bureau of Agricultural and Resource Economics and Sciences Agricultural Commodities Report from March 2024, increased cattle slaughter and beef production are expected to lead to a 21-percent increase in exports during their 2023–24 marketing year (July–June).

The chart below compares year-over-year percent changes in exports from the United States and Australia in January 2024 for the top Asian markets and the world. Exports from Australia have increased to nearly all major markets, and the country’s increase in total exports to the world was largely driven by increased exports to the United States. Decreased domestic beef production in 2024 will likely continue to push U.S. beef prices higher, making it even less price- competitive on a global scale. The forecast for U.S. beef exports in 2024 is unchanged from last month at 2.785 billion pounds, which if realized would be an 8-percent decline year over year.

January Beef Imports Leap to the Top of the Record Books

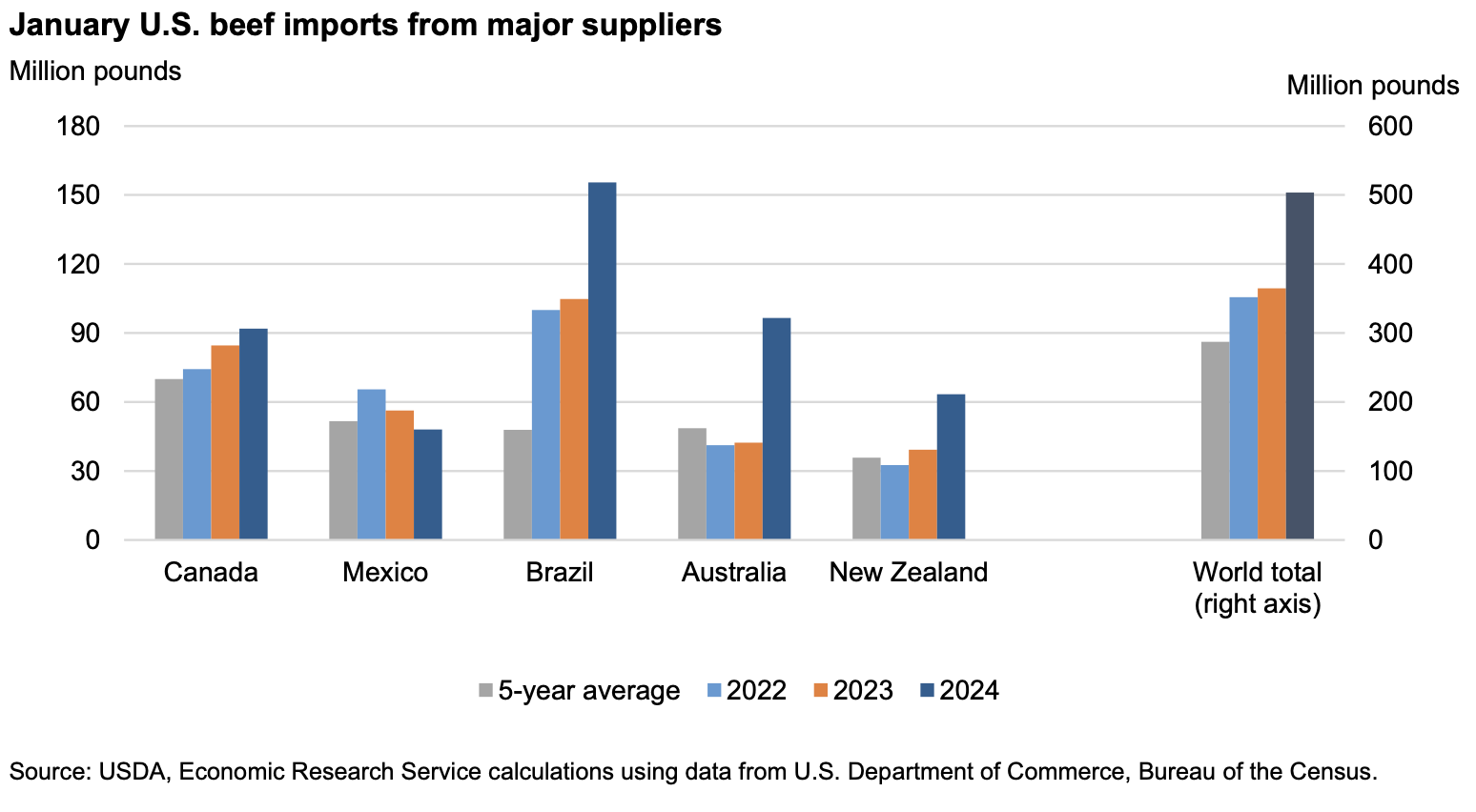

U.S. beef imports in January 2024 shattered every previous monthly record, which was not wholly unanticipated given expectations of Brazil racing to fill the “other countries or areas” tariff- rate quota. For context, the previous record for monthly beef imports was in June 2005 at 378 million pounds; January 2024 came in at 504 million pounds, 33 percent higher than the previous record and 38 percent higher than 2023. Monthly imports from nearly all major suppliers ranked in the top 10 for the month of January, but the two countries that most strongly drove the record-setting imports were Australia and Brazil.

The chart below shows January 2024 imports from major suppliers compared to the previous 2 years and the 5-year average. In January of this year, imports from Australia were more than 128 percent higher than the previous year. Shipments from Australia have increased since mid- 2023 as beef production in the country has risen. Although higher than the previous few years, January imports from Australia were lower than in 2015, when imports were elevated due to the opposing effects of the two countries’ stages in the cattle cycle: the United States with less beef production due to herd rebuilding and Australia with higher production from drought-induced herd destocking.

At nearly 155 million pounds, January imports from Brazil were, as expected, an overall record from the country. This was 48 percent higher than January 2023. Beef imports from Brazil fall under the tariff-rate quota for countries without a specific quota or free-trade agreement. This quota is set at just over 65 million kilograms, or 143 million pounds; once filled, imports face a larger out-of-quota tariff. Last year, imports from Brazil spiked in the first few months until the quota was filled and then tapered off throughout the rest of the year. A similar pattern could occur this year. The U.S. Customs and Border Protection Quota Status Report from March 4 shows the tariff-rate quota for “Other” countries is already completely filled.

As a result of the slightly stronger-than-expected January import data, the first-quarter forecast for 2024 is raised 50 million pounds to 1.200 billion, which would be another overall record quarter and a 26-percent increase over the previous year. The forecasts for the rest of the year remain unchanged for an annual forecast of 4.175 billion pounds.

4The five-area marketing region includes Colorado, Iowa, Kansas, Nebraska, New Mexico, Oklahoma, and Texas.

{kind=link}