Source: Government of Alberta

“Livestock cash prices and futures contract prices tend to move in similar patterns,” says Ann Boyda, provincial livestock market analyst with the Alberta government. “This correlation between the 2 markets lends value to the role of futures markets in price risk management.”

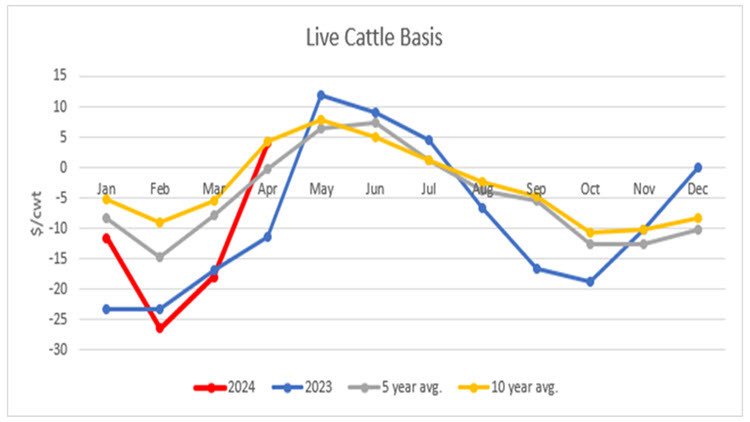

Commodity futures market price quotations reflect the collective opinion of many traders as to the upcoming supply and demand conditions. It is often described as a ‘benchmark’ market. The basis refers to the price difference between the cash price and the futures price.

Cash Market Price – Futures Market Price = Basis

The basis can be positive or negative. Negative basis implies a local cash price lower than the futures market price; and conversely, a positive basis implies the cash price is greater than the futures market price or trading at a premium to the futures.

“Generally, cash prices tend to be more volatile than the basis,” explains Boyda. “Historic basis information can help provide an estimate for forecasting prices. Feeder and live cattle basis are not constant throughout the year due to seasonal patterns in production.

“For example, with a majority of the cow herd on a spring calving system, supplies of weaned calves are greatest in the fall and ready for slaughter the next summer. Thus, feeder cattle basis is strongest in spring and typically weaker in fall to early winter, whereas live cattle basis is stronger in spring and summer. Historical basis data can be used as an indicator to help forecast future basis levels.”

Figure 1. Live cattle basis

“Even though the cattle market remains high, it is interesting to note the volatility that is evident in the cattle futures trading. Live cattle and feeder futures demonstrated a wide price range through the week of April 29.”

The market swings in large part were attributed to the news of avian influenza cases in dairy herds, leading many to perceive a risk to the beef sector. No virus has been discovered in meat and there has been no discovery of highly pathogenic avian influenza (HPAI) in beef, even in herds of proximity to dairy cases. The recent futures market prices appear to be acknowledging the lower risk and show signs of rebounding.

A closer look at the weekly percentage change in CME live cattle futures prices for the contract month closest to expiry (nearby) reveals the volatility experienced over the last year. More volatile prices imply a greater degree of risk. The annual standard deviation of live cattle future contract prices estimates 2023 volatility being the highest over the last 5 years, except for 2020.

The COVID-19 pandemic resulted in disruptions to the 2020 cattle markets stemming from packing plant shutdowns and corresponding supply chain impacts. 2023 witnessed record highs in fed cattle prices but live cattle futures moved lower in November and December, contributing to the market swings.

“Recent volatility is associated with consumer demand risks due to the avian influenza discovery in dairy cattle,” says Boyda. “USDA surveillance is alleviating some of the concerns. On May 1, 2024, USDA’s Food Safety and Inspection Service (FSIS) announced results from its testing of retail ground beef. FSIS collected 30 samples of ground beef from retail outlets in the states with dairy cattle herds that had tested positive for the H5N1 influenza virus. All samples tested negative.”

The U.S. Food and Drug Agency (FDA) announced additional results from a national commercial milk sampling study which included 297 total retail dairy samples. Testing did not detect any live, infectious virus and pasteurization was reported to be effective in inactivating HPAI.

“Seasonal trends generally are a reliable tool for forecasts, however the volatility in the futures markets demonstrates vulnerabilities. The cattle market has demonstrated strong demand in the early months of 2024 and combined with the low cow herd inventories, the feeder market should remain strong as feedlot operators strive to maintain capacity,” says Boyda.

{kind=link}