Source: FCC

As we start the new year amid elevated inflation and major headwinds facing the economy, here are our top charts to help make sense of the economic environment for farm operations, agribusinesses and food processors.

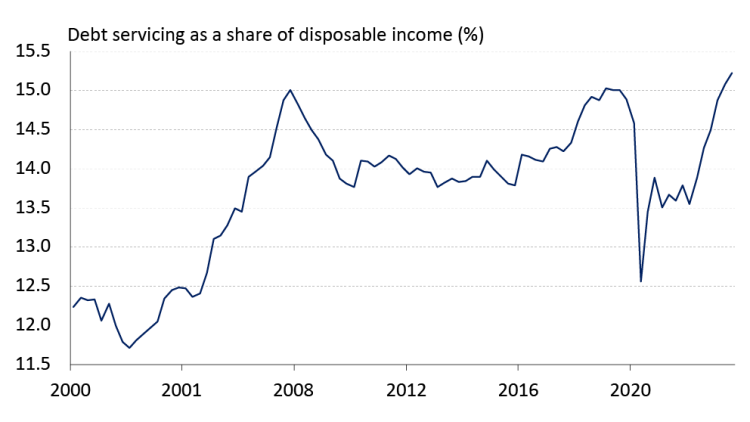

A second consecutive year of weak growth is in the cards as the impacts of earlier interest rate increases are felt more acutely throughout the Canadian economy in 2024. Consumption spending, which accounts for nearly 60% of GDP, should see a marked deceleration as households struggle under the weight of record high debt servicing (Figure 1), elevated shelter costs and a more challenging labour market.

The economic slowdown will reinforce the downtrend in inflation, causing long bond yields, and ultimately longer-term rates on fixed rate loans, to drop further in 2024. In contrast, short yields should be anchored by the Bank of Canada’s decision to keep its overnight rate unchanged for another few months. But once the central bank is convinced that the inflation downtrend is sustainable, which we’re expecting to happen around mid-year, look for it to start cutting its overnight rate to boost a flagging economy.

Source: Statistics Canada

Canada’s canola crushers set a record in the first quarter of the 2023/24 marketing year as new capacity came online (Figure 2). Canadian canola crush expansion was initially slated to add 4.5 million metric tonnes in 2024 however, rising construction costs, higher interest rates, and tight canola supplies the last several years have led to delays in projects. Increased canola crush may help swing acres to the crop, although the soybean to corn futures ratio will still be the global bellwether to understand trends in seeded acres. U.S. producers will have incentives to plant more soybeans at the expense of corn acres if the ratio stays at today’s level.

Source: Statistics Canada

The North American beef herd is going to be smaller on January 1, 2024, compared to a year earlier. Even strong prices have not been able to stem herd reductions as producers have dealt with droughts in 2 out of the last 3 summers, with heifers and cows accounting for 51% of slaughter in 2023 (Figure 3). Provided 2024 provides bountiful rain for hay and pasture, rebuilding the herd will be a multiyear process as when looking back through time the high prices during 2015 and 2016 only resulted in herds staying flat.

Sources: Statistics Canada, USDA, FCC Calculations

The USDA is expecting Canadian pork production to decline a further -1.2% in 2024 as the world faces a current oversupply of pork. Producers around the world continue to be pressured on margins leading to herd reductions, including the world’s largest producer, China. Canadian producers are going to face tight margins until at least the summer although there has been increased demand for pork domestically as consumers are shifting consumption patterns to lower priced protein options.

Source: USDA PSD

With input costs stabilizing, dairy margins in 2024 should improve compared to the last few years with current estimates comparable to margins in 2019. Feed availability and pricing – which have been extremely volatile in the last three years – will be the ultimate determinant of profitability. A bountiful U.S. crop in 2023 sent corn futures tumbling to a three-year low. With corn being the market-maker in other feed grain markets, this put downward pressure on feed wheat and feed barley costs as well, even in western Canada where drought limited production. A +/- 10% change in purchased feed costs can swing overall profitability by +/- 40%. To get a sense where the price of corn is headed in 2024, producers will want to keep an eye on corn production estimates from South America and on prospective plantings of corn in the US this upcoming growing season.

Sources: Statistics Canada, USDA

Declining crop prices and elevated farm input prices notably fertilizer have been on the minds of Canadian farmers. Our fertilizer affordability index is a top chart to monitor. The ratio between fertilizer and crop prices is an indication for fertilizer affordability, calculated by the price of fertilizer divided by the crop price. It highlights the relationship between fertilizer prices and crop prices, or simply inputs and outputs.

Our fertilizer affordability index based upon the major crop rotations has improved for both canola-wheat and corn-soybeans due to weaker global fertilizer prices relative to crop prices. The lower the ratio, the more affordable fertilizer becomes relative to the crop. Overall, the fertilizer affordability trends indicate optimistic 2024-25 crop profitability. Nitrogen has shown improved affordability across most major crop commodities. Spring wheat and canola prices have held up the most relative to nitrogen prices contrasted to corn. The ratio of commodity prices relative to the price of phosphate is also expected to improve despite more upside potential for global phosphate prices in 2024. We will continue to monitor fertilizer affordability as spring planting approaches.

Source: Alberta farm input prices, Statistics Canada, and FCC calculations

The farm equipment industry has faced supply chain issues for several years which impacted delivery of equipment from manufacturers. Reduced deliveries coupled with strong demand for farm equipment reduced inventory levels of both new and used farm equipment in 2022 and into 2023.

Supply chain issues are largely behind us and deliveries from manufacturers continue to arrive. As such, inventory levels are expected to increase in 2024. Rising inventory levels of new equipment will spill over to the used equipment market.

Inflationary pressures on new equipment prices along with higher borrowing costs are expected to slow farm equipment sales. Elevated interest rates have resulted in more caution as producers delay purchase decisions until interest rates stabilize or fall. Operations place a large focus on the cost per acre of equipment in relation to overall total costs on the farm.

Source: Association of Equipment Manufacturers (AEM) and FCC calculations

Contributors:

Leigh Anderson, Senior Economist

Graeme Crosbie, Senior Economist

Justin Shepherd, Senior Economist

{kind=link}