CME: Live Cattle (LE), Lean Hog (HE)

Last month, the Bureau of Labor Statistics (BLS) reported that US inflation on food items was 5.7% in June, exactly half of its peak of 11.4% in August 2022. Food inflation is at its lowest level since November 2021.

Under the sub-category “Meats, poultry, fish, and eggs” from Food-at-home, the BLS data shows a negative 0.2%, meaning that meat prices declined in the past year.

The official data contradicts my own experience. Anyone who has been shopping knows that the grocery bill gets bigger every month. Last weekend, I surveyed the Beef section at a local Walmart and found the following:

- Beef cuts with the USDA Choice label price between $12-$18 per pound.

- A primal loin, for example, costs $16.99/lb.

Next to Beef is the Pork section.

- A full slack of spareribs prices at $1.89/lb.

- This is back to the pre-Covid price level.

Why is beef so pricy? Will consumers get some relief as food inflation goes down? In this report, I attempt to find out what drives the beef/cattle price up.

The Cash Cattle Market

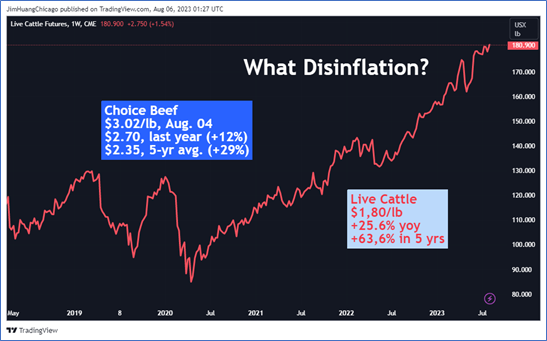

According to the National Daily Cattle & Beef Summary published by the USDA, Choice Beef averaged $301.79/cwt (per 100 pounds) nationwide on August 4th. Primal loin cutouts averaged $4.11/lb. This is so much lower than the retail price. But why?

The USDA reports transactions occurred at meatpackers, where cattle farmers sell their beef cows. The report shows the value chain throughout the packing process:

- Live Cattle: Steer (male cow), 187.55/cwt; Heifer (young female), $187.26/cwt;

- Beef Carcass: $284.86 (Choice);

- Primal Flank: $214.84 (Choice);

- Primal Rib: $457.54 (Choice);

- It also lists prices for Chuck, Round, Brisket, Short Plate, Trimmings, etc.

From the packing plant, beef goes through cold storage, wholesale, and retail distribution before consumers pick up their favorite meat at the grocery store.

During the inflationary period, labor and energy become more costly, driving up the cost of each stage of processing and distribution. Higher interest rates also raise the cost of business overhead. These together widen the price spread between live cattle and retail beef cutout significantly.

In the beef cattle value chain, it takes farmers two years to raise the cows, while processing and distribution take maybe two weeks to complete. However, farmers receive only about 20% of the final sales price.

The Cattle Cycle and A Shrinking Herd

Cattle cycle is the process in which the size of the national cattle herd changes over time. The cattle cycle averages 8–12 years and is influenced by the cattle prices, input costs that drive producer profitability, the gestation period, the time needed for raising calves to market weight, and climate conditions.

If cattle prices and producer profits are expected to rise, producers may expand their herds; if prices are expected to decline, producers will reduce their herds by culling older cows and keeping fewer heifers to replace older cows.

Cow-calf producers’ response to price fluctuations may be delayed because of the lengthy gestation period for cattle relative to hogs and poultry. The total number of beef cattle in the United States is highly dependent on the stage in the cattle cycle.

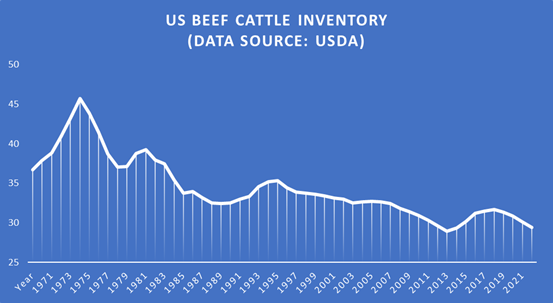

Last month, the USDA reported that the latest herd inventory for all cows and calves was 95.9 million, down 3% year-over-year. Beef cow inventory was 29.4 million, also down 3%. The decline in beef cow supply is the main driver for higher beef prices.

Over the past 50 years, the US cattle herd has shrunk significantly.

- Inventory for all cows and calves peaked at 132 million in 1975. We have lost over 36 million cows or 27% of all cattle supply.

- Beef cattle inventory peaked at 45.7 million. We now have 2/3 of peak herd size.

A counter argument is that, with technology advancements, we need fewer cows for the same amount of beef supply. The production time gets shorter, and the cows gets bigger. People now have healthier diets and take in less red meat.

According to USDA data, per capita beef consumption was 63.3 pounds in 1960. It declined to 59.1 in 2021, down 6.6%. But look at the huge population growth for people. The US had 203.2 million people according to the 1970 Census. US population grew to 331.4 million in the 2020 Census, up 63%.

Beef Export and Import

Interestingly, the US both exports and imports beef. In 2021, the US exported 3.43 billion pounds of beef while imported 3.35 billion pounds. Beef export was mainly higher-grade beef cutouts. And import was lower-grade beef for processing into ground beef.

The US used to be a net import country for beef. In 2020, China signed a trade agreement with the US and opened its vast market for US beef import. This resulted in China buying four times as much beef the following year.

More export reduces domestic beef supply. This is another factor driving up beef prices.

In conclusion, the days of lower priced beef are long gone. Beef prices are expected to remain high, even though food inflation goes down.

Cattle and Hog Spread Trade – A Revisit

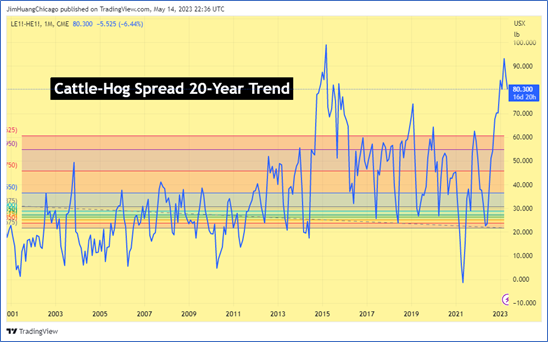

How could we make use of this analysis? On May 15th, I published an idea about spread trade between CME Live Cattle Futures ($LE) and Lean Hog Futures ($HE).

The 20-year chart shows that the price spread between live cattle (LE) and lean hog (HE) broadly stays in the range of $20-$60 per 100 pounds but could go up to as high as $100.

On May 12th, October cattle contract (LEV3) was quoted $166.2 per 100 lbs., while October hog contract (HEV3) priced at $77.425. Thus, the price spread was $88.775.

On August 4th, LEV3 settled at $183.10 while HEV3 was closed at $83.25. The spread has widened to nearly $100.

The Impact of Proposition 12

In 2018, California passed an animal welfare law called Proposition 12. It requires that breeding pigs be confined to a pen with no less than 24 square feet of floor space, allowing them to fully turn around in their living area.

Proposition 12 applies to not only hog farmers in California, but also any supplier selling hog and pork in the state of California. The hog industry fought hard but lost. The Supreme Court upheld the law in May, and it is finally taking effect in July.

The animal welfare law significantly increases the cost of hog production nationwide. Prices of live hog, pork cutout, ham and bacon shall all go up. However, as we are now in summer, a low pork consumption season, cash market price has not yet caught up.

In my opinion, the cost factor pushing pork prices up in the short run is greater than the supply-demand force that drives up beef prices in the long run. There may be room to short the cattle-hog spread, until pork prices stabilize in a new equilibrium.

A Short Spread trade entails selling 1 CME Live Cattle Futures and buying 1 CME Lean Hog Futures. Both contracts are based on 40,000 pounds of meat and require $1,600 in initial margins.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trading set-ups and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs https://www.tradingview.com/cme/

{kind=link}